Central Banks Continue to Fight Inflation at the Risk of Economic Growth.

Central Banks Continue to Fight Inflation at the Risk of Economic Growth.

Reserve banks take on a marathon of interest rate hikes that continue to put pressure on financial market asset prices, businesses and individuals.

Hello friends. A warm welcome to new readers and subscribers. I am glad you are here!

The current macro conditions of tighter monetary policy inducing inflation continue to impact asset prices across all boards negatively while giving the US dollar dominance in the foreign exchange market. Although this might impact economic growth negativley in the short to medium term, it provides a good opportunity for investors to get on to long term value that has been affected by short term cyclical market conditions.

Today at a glance:

Reserve banks take on a marathon of interest rate hikes that continue to put pressure on financial market asset prices, businesses and individuals. A deep dive into each asset class.

The threat this and other socio-economic along with geo-political developments pose on the global economy.

We are currently going through a period where the cost of borrowing is increasing aggressively. In their battle against Inflation, central banks are increasing interest rates which such action as we recall has the effect of decreasing the amount of money chasing goods and services by incentivising saving and punishing borrowing (higher interest rates).

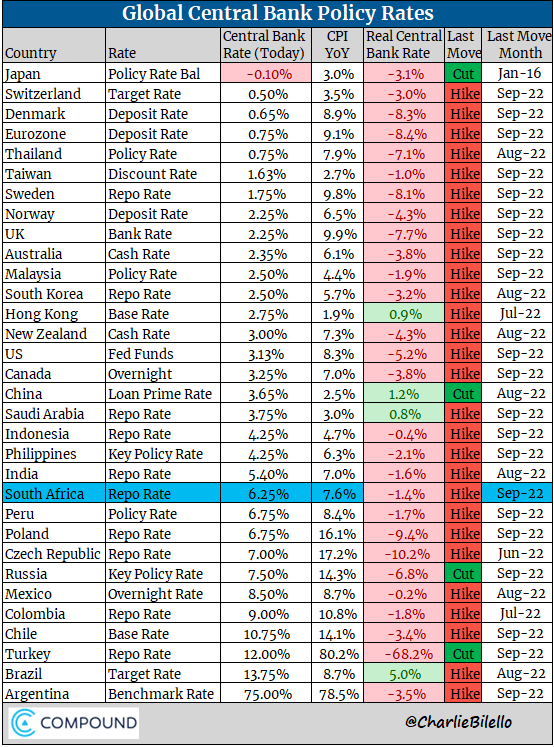

The graph below shows an update of the recent central bank rate hikes we witnessed the previous week, with a few variances of central banks that cut rates.

Asset prices have been hampered across the board:

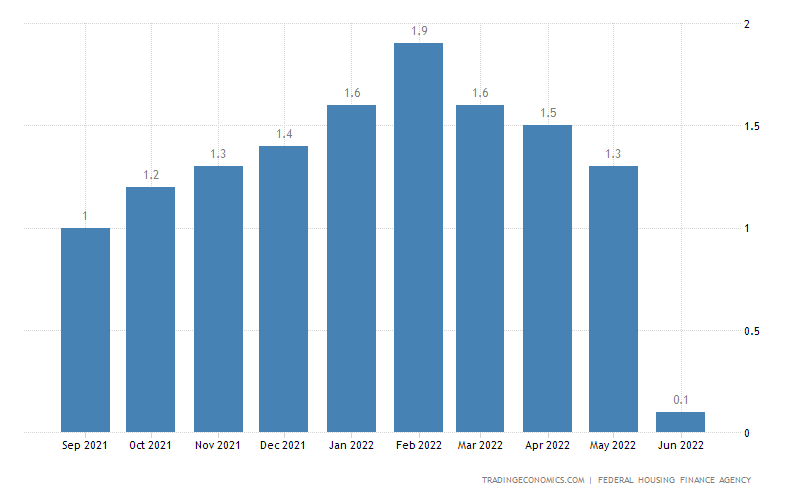

Housing - US

The housing market (using the US as a proxy) has been hit badly along with most asset classes. From the graph above, the US 30 year mortgage rates have accelerated up due to higher interest rates.

When the cost of financing an asset purchase increases it becomes likely that demand for the underlying asset will decrease and that is what we are seeing in the US with the US price housing index showing signs of slowing down due to lower appetite for housing.

Before starting the decline trend at the beginning of the year (which was around the time central bankers started tightening interest rates), the US housing market was at a historic peak.

See the graph below which shows the decline in housing prices month on month.

Bonds

Bonds have been constantly sold-off this year and that has continued in the latest monetary policy tightening rounds. Typically, investors won’t hold bonds when they expect high inflation because bonds return fixed returns meaning rising inflation threatens the purchasing power of those fixed returns, hence the yields on bonds have increased further in the past week as bonds get sold - off

Special case - England

Bonds have been sold-off in England after British Chancellor of Exchequer Kwasi Kwarteng announced the UK's biggest tax cut in 50 years which meant a government that is already in a budget deficit will be receiving less revenue from taxes, implying a higher deficit which led the market to believe they have to borrow more (sell more bonds) to fund operational and capital expenses.

The market did not want to hold England's bonds on the fear that the English government would take on too much debt so much so they would not be able to pay the debt back.

Equities

Equity valuations have also been impacted negatively globally considering that equities are sensitive to changes in bond yields which are both used as the risk free rate in valuing them and weighted average cost of capital (WACC) to discount future cash flows. A higher WACC discounts these cash flows at a higher rate hence lower valuations.

Considering that markets are forward looking, when there is an expectation that bond yields will increase, equities will price that in real time.

USA (S&P 500)

EUROPE (STOXX 600)

SA (JSE ALL SHARE)

Crypto

Keeping in mind that the crypto market has been closely positively correlated with equities under the grouping that they are risk - on assets , crypto has been negatively sensitive to higher interest rates

While central bankers’ actions (especially the US FED) are key to watch, bitcoin is still a fundamentally different asset class to equities, looking at bitcoin native data in conjunction with the FED’s actions is key. What I am watching these days is the relationship between short term holders (STH) and long term holders (LTH) of bitcoin.

Typically LTH buy at low btc prices and start selling some of their positions at high valuations (typically the convicted market players that understand the fundamentals of the asset), whereas STH buy at rising prices (mainyl due to FOMO) and sell when the price decreases (more than not due to lack of conviction).

The two graphs below show these relationships well.

This is important because in a bear market (decreasing asset prices) the point where STH sellers have less strength than LTH buyers is that where the price of the asset will not decrease any further because it is starting to pick up stronger demand (LTH) than supply (STH)

Will clemente shared it so well in one of his tweets recently; the cost basis (the average price these groups have bought their BTC) of LTH fell below that of STH meaning the asset is starting to gain demand from stronger hands (LTH) at its current market price which tells us there is a strong enough demand that any further supply will be picked up efficiently by buyers to maintain the price as is or drive it up as economic and market conditions clear.

Typically it takes up to a year for the uptrend to start building up and looking at the current economic conditions of high inflation coupled with monetary policy tightening, we could have actually reached a bottom if inflation peaks within the next two quarters, we could see monetary policy easing, bringing back liquidity into the market which will be good for bitcoin and crypto.

I tend to follow the school of thought that bitcoin is a hedge against monetary policy inflation rather than consumer price inflation hence when monetary policy is tight btc should perform badly and vice versa when monetary policy is easy btc should outperform and be a hedge.

Foreign Exchange

The US Dollar continues to be the global fx market wrecking ball, gaining constant momentum to the upside. These are the perks of having more than 60% of the globe's biggest asset class (debt) being dollar denominated and the dollar's structural dominance which always leaves the world in demand of dollars.

What we have learnt from history is that the fabric of each country’s monetary policy actions are‘threaded’ with an underpinning synchronicity to create a unified global monetary policy moving in one direction.

The highs and lows of high employment, high demand, and hot inflation, where the economy needs to be slowed down and the lows of low employment, sloging demand and deflation, where the economy needs to be jacked up, happen at almost the same time.

To the extent that when North America has a set of economic conditions, Europe has those too, so does Asia, and so does Africa. Whilst there are variances this leads to synchronised monetary policy.

The graph shows that global monetary policy is correlated. In simple terms, meaning that the supply of respective currencies is increased and decreased almost at the same time periods, yet whenever that supply changes, for increased supply, the US dollar gets less weaker, and for decreases in supply it gets parabolically stronger relative to other currencies which we are seeing the play out of this relationship best this cycle.

Final words.

These are tough conditions globally and the respective impact they have on each asset class spills out to place a big threat on the global economy. Factor in the respective issues each region or country is facing, the risk is further exacerbated.

Businesses are struggling: (a) Funding operations is difficult since there is less capital available for them and the capital already on their balance sheet is getting more expensive to service (both on the debt and equity market via bonds and equities) (b) dollar denominated expenses are hurting profit margins and (c) supply side inflation of shortages in energy which is murdering margins.

We are starting to see the first order effects of this, in the US companies are starting to retrench employees to cut costs who themselves are in trouble with high cost of living from high mortgages, high food prices and petrol prices which further threatens government tax returns.

This has the strong feedback loop of parabolically strengthening an economic demise in the medium to short term.

Although we may be in stormy conditions I have never been more optimistic. The conditions provide a good opportunity for investors to get on to long term value which has been affected by short term cyclical market conditions.

Talk to you soon.

-Kusa Nkosi