How Bond Yields Are an Important Determinant of Equity Valuations.

How Bond Yields Are an Important Determinant of Equity Valuations.

Hello Friends. I am glad you are here. The financial markets have taken huge strains lately, continuing a down trend we saw develop momentum at the start of this year (2022). A lot of factors are at play, one of the most important to market participants - Interest rate hikes globally, which have affected bond yields.

Today at a glance

- How bond yields are an important determinant of equity/stock valuations.

Bond yields have been typically used by analysts and investors as an important lead indicator to gauge the direction of equities. While there are exceptions, the equity markets have usually moved negatively with bond yields. That means as bond yields hike, equity markets tend to plummet, and as yields decrease, equity markets tend to surge to high levels. This relationship is mostly visible between the 10- year treasury bond yields and equity market indexes.

So, let us take a few steps back

What are bonds?

What are bond yields?

What are equity indexes?

Bonds are a publicly tradable asset class that you and I can buy as an investment. They return an agreed upon fixed return, and interest rate, also known as the coupon rate, at certain intervals for a given period, of which at the end of that period - at maturity date,we get the initial investment back - also known as the ‘principal’

There are various types of bonds, and institutions that issue bonds – but for today, I will I be referring to government bonds (treasury bonds) which the government issues, for investors to buy, as a means of raising capital for maintining and optimizing the socio-economic status of the country.

Let’s consider an example: The South African government issues a 10-year bond worth R1000 returning R100 ,10% per annum - What this simply means is that you and I have an opportunity to invest R1000, give it to the government in return that we receive a R100 return (10% of R1000) every year for ten years, and at the end of ten years, we get the initial R1000 back.

As you and I would know, bonds are not the only asset class, meaning as an investor, one has many asset classes to choose from, and the government is always in competition to provide bonds that return a high interest rate to attract investors.

So, in a market where returns across other asset classes, like equities, mutual funds and commodities are high, the government will have to issue out bonds that have higher if not competing interest rates.

This means if returns surge the governemnt will start issuing bonds that have higher returns than those they had issued prior returns having risen accross the market. This brings an intersting dynamic within the two sets of bonds ( prior and post return increase) issued by the government.

‘Bond 1,’ worth R1000, issued at a 10% interest rate, will be a less favourable bond investment if the government has issued the same bond at 12% (in an attempt to keep up and attract investors) interest rate = ‘Bond 2’

As Bonds can be traded publicly , if I have bought ‘Bond 1’ from the government and a day later due to increasing competition in asset classes, the government issues ‘bond 2’ , my bond will be less attractive compared to the new bond 2 in issue because it is at the same price, but offers a lower return and lower interest rate. Bond 1 has a return of R100, while bond 2 is returning R120 ,as a result in order for my bond to be attractive to market participants, should I want to sell it, it has to be priced lower than R1000 so that it yields 12% return . It currently has an interest rate of 10%.

To do that it will have to drop to R833. The return is fixed at R100, but the price has slipped to R833. Although the interest rate on this bond is still 10%, the yield has changed and no longer 10%, but now 12%

Yields are calculated as (yearly return/ Current price of bond) x 100.

So, for the bond 1 at the new price of R833 which is in level competition with bond 2 ,has a yield of R100/R833 =12%. The yield shows us what the return on investment will be from a bond, if a market participant buys it at it’s current market price.

Lastly, equity indexes are a group of equities/shares composing one instrument that can be bought on the equity market. Each share carries a weight on the index. Since indexes, like the S&P 500 Index, Nasdaq Composite Index JSE all share represent an extensive portion of the equity markets in their respective equity markets (JSE/Nasdaq/NYE), I will use them to illustrate the relationship between equity markets and bond yields.

Now that we are clear on bonds, yields, and indexes, here are the important causal effects of the negative correlation relationship between bond yields and equity markets

Bond yields are the opportunity cost of equity investments

Bond yields are the opportunity cost (amongst others) of investing in equity - they are the forgone, sacrificed return if one invests their funds in equities. The opposite holds, equity returns (amongst others) become the forgone return -opportunity cost of investing in bonds.

For example, if the yield on a bond is 6%, the lowest return on equities for them to be attractive to investors is 6%, however considering that equites are riskier, we will have to add a risk premium which would be 4% and the overall return for equites would be 10% for us to consider them in line with bonds - as a result when it occurs that equites are having lower returns than bonds, e.g. 9%, or investors’ expectations is that equity returns will be lower in the immediate to mid-term future, bonds will be more attractive and investors will flog to buy bonds.

Bond yields impact the cost of capital in valuing equities

This is the most important causal effect, a big reason why investors are keeping a close eye on the 10- year US treasury yield, which hit 3.17% for the first time since 2018 the previous week. The South African 10- year government bond yield has also seen increasing yields, sitting at 9.99%. In both countries, the equity markets have been affected by the increase in bond yields

Yield on bonds is normally used as the risk-free rate when calculating cost of capital. When bond yields increase, so does cost of capital. This means that a company’s future cash flows get discounted (present valued) at a higher rate, lowering the present value of future cash flows resulting in flattened equity valuations.

Increasing bond yields impact financial costs.

When bond yields increase it is a lagging indicator for higher cost of debt, meaning corporates face higher interest rates, interest payments on the loans they have taken out. This reduces company’s cash flows and earnings, and ultimately this is not good for market sentiment, selling of equities will occur and equity valuations will drop.

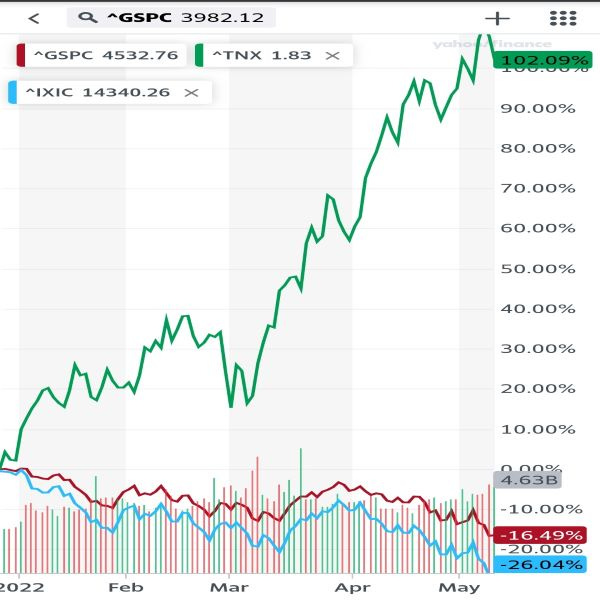

Red=S&P 500 index

Blue= Nasdaq composite index

Green =10-year US treasury bond yield

With the understanding of the causal effects, the relationship between yields and equity valuations becomes eye catching.

This graph depicts the relationship between the 10-year US treasury bond yield and the S&P 500 Index as well as the Nasdaq Cmposite Index (as proxies for equity valuation), from 1 January to 13 May (2022) (Year To Date- YTD). The Bond Yield is Up 102% while both the S&P 500 Index and Nasdaq Composite Index are down 16 and 26 (%) respectively – negative correlation in play, when yields increase, equity valuations plummet.

Thank you for reading Curiosity. This post is public so if you found it insighful feel free to share it

Other equity market developments I had my eyes on this week:

Thank you for being here friends. Talk soon - Stay Curious

-Kusa Nkosi

Every Thursday evening I string a few words and data sets together to put up my favourite love letter. Cuddle up with all my other friends to read my personal opinion on: Global Fintech-Economics | Crypto | Blockchain | Mental health every friday evening