Private Equity Going Concerns

Private Equity Going Concerns

It is no secret that many private, venture backed companies raised capital in the previous bull run at overinflated valuations that could see significant corrections in 2023.

Hello friends. A warm welcome to new readers and subscribers. I am glad you are here.

While major global public markets have in part efficiently priced in deteriorating investing conditions (high interest and inflation rates) across different asset classes and markets, the private equity market hasn’t, and as investors expect better investing conditions in 2023, there is still more pain to be experienced in private equity.

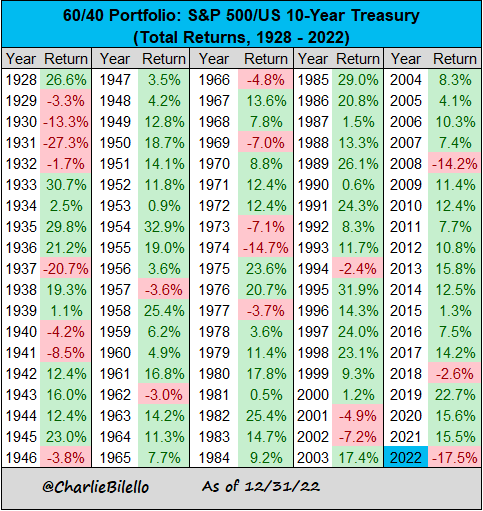

The S&P 500 ,as a proxy for the US public equity market, was down 18% in 2022, its largest valuation drop since 2008, 4th largest since 1940. In correlation to public equity was also the (US) bond market which had its worst drop in history at 13%, making harvesting returns for the typical 60/40 portfolio impossible in 2022, at a loss of 17%, the worst return since 1937 (chart below).

As inflation is increasingly expected to ease lower by analysts, conditions fare better for investors to get on to sound public companies whose valuations have been impacted by cyclical market conditions with a similar opportunity opening up in the bond market.

Although 2023 might present tougher economic conditions, with the possibilities of a global recession (negative economic growth) becoming less and less remote, public markets are forward looking and on the expectation of lower interest and inflation rates could bid up public assets, hence a turnaround in markets is likely albeit bad economic conditions.

Inconsistent to public markets, specifically the public equity market, is the private equity market (companies that are not listed on public trading exchanges) whose valuation adjustments are stickier than public market, mainly because private equity firms that drive investment in the private space have a bias to defend high valuations of the companies they invest in so as to prevent realizing losses that will drive down profitability, and valuation when raising capital for investment.

As VC firms face reality (evidently well after long public investors have), they will mark these unprofitable high valuation companies funded companies to zero book value from uncommonly valued going concerns.

The graph below shows the lag in private equity valuations (Prime Unicorn Index) against public equity valuations (Renaissance IPO Index).

This was the case as well back in the 2000 dot com bubble where the private equity market lagged its counterpart public market, both in the bubble and bust.

It is no secret that many private, venture backed companies raised capital in the previous bull run at overinflated valuations that could see significant corrections in 2023 as reality strikes for private equity investors, and as the public market pents-up an upside turnaround, the private space is likely following economic growth downwards.

Talk to you soon!