The Unravelling of First Republic Bank: A Cautionary Tale for Small US Banks.

The Unravelling of First Republic Bank: A Cautionary Tale for Small US Banks.

Hello friends. A warm welcome to new readers and subscribers. I am glad you are here!

When reserve banks started raising interest rates and taking on quantitative tightening to fight inflation, it was widely accepted that soon, something within the system would start breaking. Whilst there was broad consensus on the direction that risk was headed, little was evident on the speed and length towards that direction. A few rate hikes down the line and another US bank is fighting for survival. First Republic Bank's (FRB) market value is down 98% in four months. What on earth happened?!

The underlying risk FRB faced.

When rates rose, they sparked credit, interest rate and deposit risk for banks. The risk that debtors would default on debt, that fixed rate loans portfolio’s market value would collapse (being highly elevated for FRB considering that the key business model for the bank has focused on attracting high net worth individuals’ deposits using extremely low fixed rate mortgage bonds and business loans), and that money market funds that tracked short term treasury bills would offer higher yields than savings and interest yielding checking accounts, leading to depositors withdrawing their deposits from banks to high yielding money market funds. I wrote extensively on this in my previous communication.

The events as the demise was triggered.

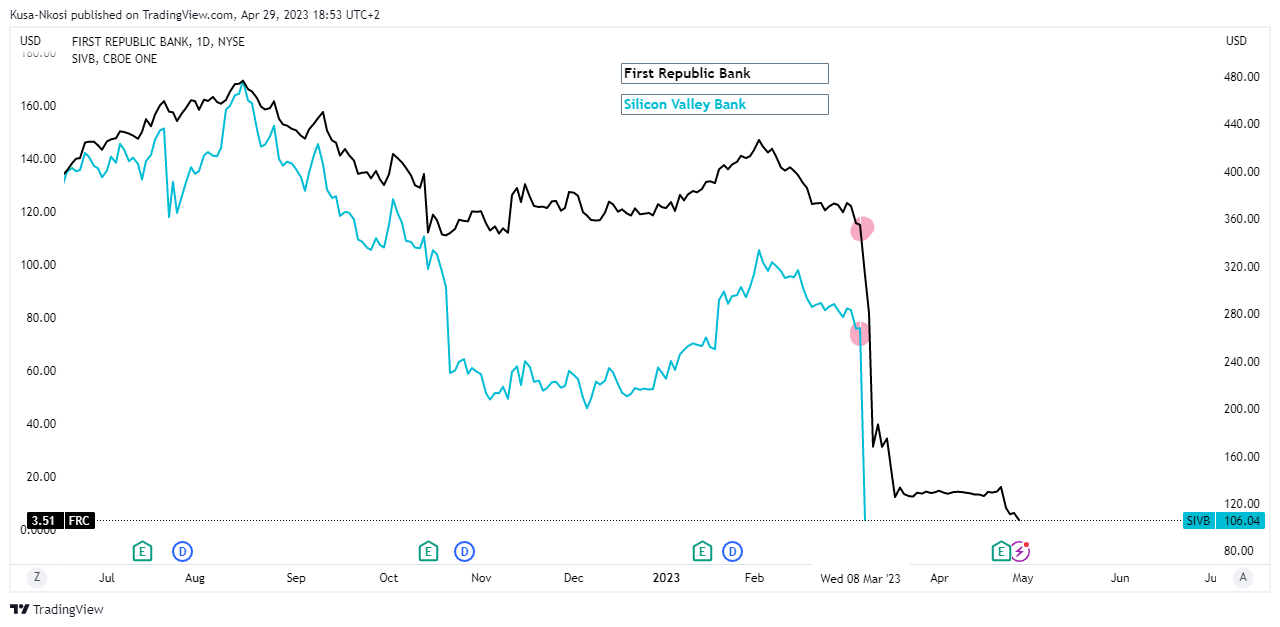

The first market value wipe out for FRB was in tandem with and largely triggered by the Silicon Valley Bank (SVB hereon) debacle, triggered by impaired customer and investor confidence, highly due to outsized losses on the bank’s fixed income portfolio and a capital raise via common share issue that left investors doubtful of the bank's liquidity.

Consequently, FRB’s share price fell 73% between the period 8 to 13 March 2023 (more than other small sized banks that saw a fall too) in similar fashion to SVB. At that point, concerns around FRB were speculative, but proved to be well found when the bank released its 2023 Q1 earnings report early this week (24 April 2023). A few highlights from the report:

The bank's deposits are down from $176.4 billion (2022 yearend) to $104.5 billion (end of Q1 2023). Excluding the $30 billion uninsured rescue deposit received from various American banks as reported on 16 March, the bank's net deposit outflow is $101.9 billion.

An analysis reported by Reuters showed that FRB had suffered the biggest percentage withdrawals in the entire financial services (banking) industry and small sized banks category in the US. At 35. 5% (including the $30 billion deposit injection) and 58% excluding.

Final words.

The risk for small sized (regional) US banks remains high as depositors continue to seek safer and higher yielding investment options, the winners; money market funds and “too big to fail” banks. Things are starting to break!

Talk to you soon!